市场资讯及洞察

.jpeg)

4 月的美股财报季正拉开序幕,而当下的市场追求的不仅仅是一个动听的故事。

正如 GO Markets 在最近的《国防股财报观察名单》中所强调的,本轮财报季标志着市场核心关注点发生了更广泛的转变。现在,投资者不再仅仅追求“不计代价的增长”,交易员们更渴望洞察潜藏在数据背后的真实信息。

为什么这三家公司至关重要?

在当前的市场环境下,特斯拉 (Tesla)、NextEra Energy 和埃克森美孚 (Exxon Mobil) 成为了焦点。它们分别代表了 2026 年的三大核心叙事:自动驾驶、电力需求以及原油供应风险。

- 特斯拉 (Tesla): 市场正在评估其自动驾驶和能源业务是否足以支撑下一阶段的增长。

- NextEra Energy: 为观察电力需求激增以及满足该需求所需的基础设施建设提供了一个窗口。

- 埃克森美孚 (Exxon Mobil): 在供应风险持续存在的背景下,处于原油与能源安全叙事的中心。

综合来看,这三家公司有助于解释市场关注点的转移趋势:现在的关键不再是谁的叙事最动人,而是谁能展现出真实的需求、更稳健的利润率,以及在日益复杂的宏观背景下依然坚韧的执行力。

在 2026 年,AI 驱动的电力需求正将公用事业、储能和电网容量推向聚光灯下;与此同时,原油供应风险也让**“能源安全”**重新回到了市场的核心对话之中。

.png)

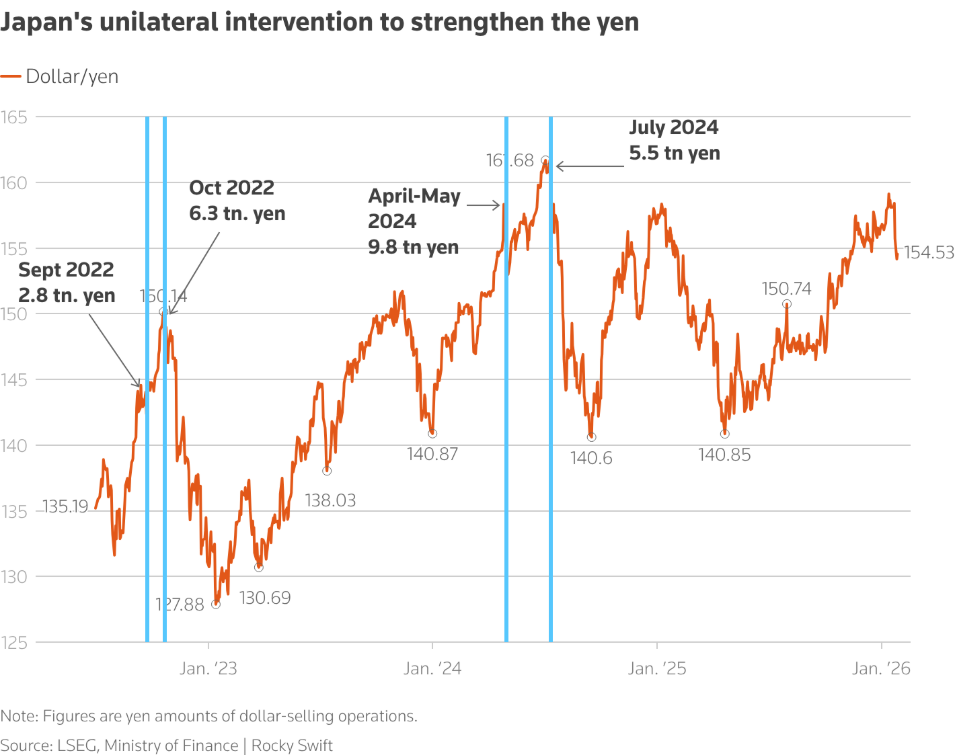

最近外汇市场发生的一件事,看起来不复杂,就是日元在一个关键位置突然稳住了。但如果只把它当成日本自己出手,可能会漏掉真正重要的部分。

日元走弱已经不是一天两天了,市场早就盯着几个重要点位。很多人心里都有数,真到那一步,例如160左右,日本大概率会有动作。所以当汇率真的被拉住时,没人会觉得意外。

意外的是,出手的不只有日本,纽约那边也有同步操作。

也就是并不是日本单方面救火,而是有人在旁边帮了一把。而这个“旁边的人”,并不是普通角色。

这件事之所以值得反复琢磨,是因为美国其实没有那么明显的理由去管日元。美元并没有强到失控的程度,过去一段时间,市场反而一直在讨论美元是不是被高估,是不是应该分散配置。在这种背景下,美国如果主动压低美元,反而显得有点多此一举。

那问题就来了,美国为什么要参与?

答案并不在汇率本身,而是在另一个大家平时不太爱盯着,但更关键的地方,美债。

可以换一种更直观的方式理解。日本如果想靠自己稳住汇率,最现实的办法是什么?动用外汇储备。而外汇储备主要放在哪里?很大一部分就是美国国债。也就是说,日本一旦大规模行动,很可能就要卖掉一部分美债,换成别的资产,再去市场上买日元。

这样一来,日元是稳住了,但美债市场就可能被冲击。债券一被卖,价格就容易跌,收益率就会上去。而这件事,恰恰是现在美国最不想看到的。

在当前环境下,美国最大的顾虑之一,就是利率再被推高。融资成本上去,不只是政府压力大,整个金融市场都会跟着紧张。所以,美国选择了一种更“省事”的方式,直接在外汇市场上配合操作,把对债券市场的影响压到最低。

这样看,这次行动的重点,其实并不是把日元拉到什么位置,而是尽量不让问题从汇率蔓延到利率。

从结果上看,这个目标基本达成了。债券市场并没有出现明显波动,利率保持在一个还能接受的区间。美元短期走弱并不意外,但也没有出现失控的情况。日元确实得到了喘息的空间,但更多是暂时的缓冲,而不是方向上的改变。

说到这里,就不得不提最近被反复讨论的一个词,去美元。

每当贸易摩擦、关税威胁或者政治摩擦升级,市场上就会出现类似的说法,好像大家都要抛弃美元资产了。但如果真的去看钱的去向,情况其实没有那么极端。

确实有一部分资金在离开美元体系,最典型的就是买黄金。黄金不属于任何国家,不用担心信用问题,这也是为什么在不确定性上升时,黄金总是容易受追捧。但这更多是部分资金的选择,而不是整体行为。

从实际的数据看,很多国家并没有大规模抛售美元资产,尤其是美国的传统伙伴。短期内可能会有流出,但市场情绪缓和之后,资金往往又会回去。原因也很现实,可替代的选择并不多,能承载大规模资金的市场,更是屈指可数。

所以,与其说现在正在发生全面的去美元,不如说大家开始更谨慎了。有人在分散风险,有人在减少单一依赖,但这和彻底离开,是两回事。

放在这个背景下,再回头看这次日元干预,就更容易理解了。它并不是在宣告某种新秩序,也不是一次激进的政策转向,更像是一次临时的稳场操作。目的很简单,把可能扩散的风险先按住。

趋势会不会改变,还要看更长时间的变化。但至少在关键时刻,有些底线,仍然有人愿意出手去守。对市场来说,这本身就是一个重要的信息。

今年金价突破5,000美元,白银飙升至100美元以上,这可能是金属交易者的历史书籍之一(不管怎样)。

事实速览

- 在年初突破5,000美元之后,避险需求的增加使黄金目标从5,400美元升至6,000美元。

- 人工智能(AI)和数据中心基础设施的建设可能有助于推动白银和铜的需求。

- 持续的地缘政治不确定性和不断变化的货币政策可能会引发全年金属波动。

2026 年最值得关注的五大金属

1。金

金价突破5,100美元,比一些预测提前了三个季度。随着美国银行迅速将其年终目标提高至6,000美元,高盛预计为5,400美元,避险商品仍然是2026年最大的关注资产。

关键驱动因素:

- 各国中央银行目前平均每月购买60吨黄金,而2022年之前为17吨。

- 美联储将在2026年进行两次降息,从而降低持有黄金等非收益资产的机会成本。

- 特朗普的关税政策、中东的紧张局势和财政可持续性的担忧使避险需求持续上升。

- 黄金在总金融资产中的份额在2025年第三季度达到2.8%,随着零售FOMO的开始,还有增长的空间。

要看什么

- 杰罗姆·鲍威尔定于2026年5月被接替为美联储主席。替代后的实际政策方向可能与当前市场对削减的预期有所不同。

- 避风港的地缘政治套期保值是否仍然存在,或者是否出现像2024年后美国大选这样的平静局面。

- 作为对美国关税的回应,欧洲国家可能将持有的美元资产武器化。

2。银

白银是从2025年人工智能繁荣中受益最大的金属,从2026年开始,白银飙升至112美元的历史新高(根据美国银行的信号,白银比基本面值高出70%),这表明了其波动潜力。

关键驱动因素

- 来自人工智能基础设施、太阳能和电动汽车(EV)、半导体和数据中心的工业需求目前无法替代银的导电性。

- 连续六年供应赤字,地上库存耗尽,回收瓶颈限制了二次供应。

- 政策视角可能很重要。美国决定将白银加入其 “关键矿产” 清单被列为波动的潜在因素,包括围绕贸易政策的风险。

- 零售参与可以放大价格走势,尤其是在对黄金的需求变得 “过于昂贵” 的情况下。

要看什么

- 太阳能电池板需求是否继续保持其增长势头,或者2025年是否达到峰值。

- 回收供应是否通过提高炼银和材料加工能力来应对创纪录的价格。

- 交易所库存和租赁费率的变化是物理紧张的潜在信号。

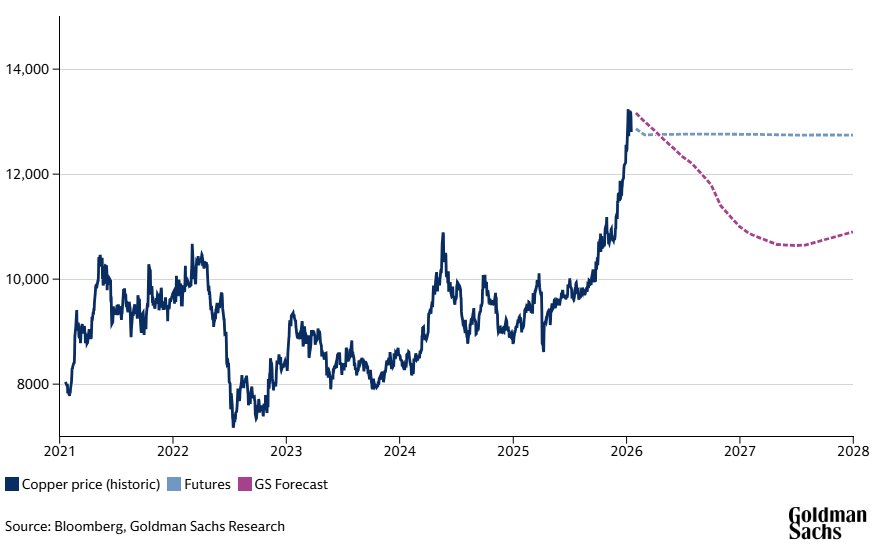

3.铜

铜业2026年的走势取决于持续的数据中心需求、可再生能源基础设施的增长以及陷入困境的中国房地产市场。

关键驱动因素

- 预计到2026年,数据中心的铜消耗量将达到47.5万吨,比2025年增加11万吨。

- 智利的工人罢工和格拉斯伯格的重启延迟使铜市场的结构紧张。

- 美国对精炼铜进口的关税决定预计将在2026年中期作出(目前预计将超过15%),这将造成潜在的库存和贸易流量扭曲。

- 高盛预测,到2030年,电网基础设施和电动汽车建设可能会增加 “另一个美国” 的铜需求。

- 当前中国房地产疲软正在造成需求的不确定性,有可能抵消基础设施支出。

要看什么

- 格拉斯伯格是顺利提高产量还是面临进一步的挫折。

- 中国房地产市场刺激的有效性。

- 实际费率实施的时间和规模。

- 洋山保费走势表明实际实际需求与财务状况的对比。

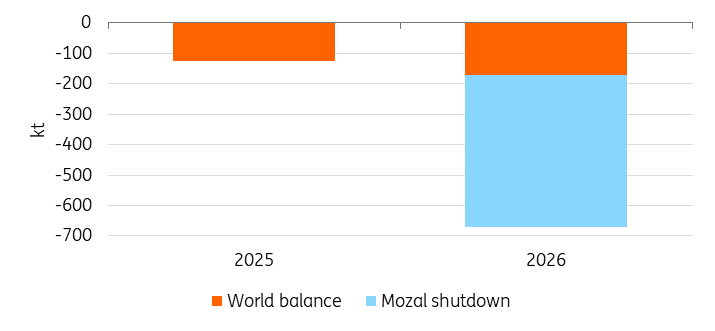

4。铝

由于中国的产能上限迫使全球市场进行调整,铝的交易价格接近三年高点3,200美元,直到2026年仍将面临持续的紧张局面。

关键驱动因素

- 中国的4500万吨产能上限是在2025年达到的。几十年来,中国的产出首次无法扩张,有可能终结全球80%的供应增长。

- 随着铜价的上涨,路透社报道说,随着相对价格的变化,一些制造商一直在某些用途中用铝代替铜。

要看什么

- South32表示,预计莫扎尔铝业将在2026年3月15日左右接受保养和维护,从而减少莫桑比克56万吨的大量供应。

- 如果印尼和中国海上产能的增加能够弥补中国国内的上限。

- 世纪铝业在第二季度重启5万吨的霍利山可能为整个行业提供信号,因为该冶炼厂预计将在2026年6月30日之前达到满负荷生产。

5。铂

铂金突破2,800美元是在连续三年供应赤字以及氢燃料电池(氢燃料电池的重要组成部分)采用率增加之后出现的。

关键驱动因素

- 世界铂金投资理事会(WPIC)预测,2026年将出现85万盎司的巨大供应赤字,这可能会耗尽库存,新增产量有限。

- WPIC预测,到2030年,重型卡车、公共汽车和绿色氢电解器的吸收量为87.5万至90万盎司。

- 催化转化器中的钯金替代品正在增加电动汽车产量。

要看什么

- 生产商的供应回应。Platreef和Bakubung正在增加15万盎司,但生产纪律可能会限制更广泛的产量。

- 美国对俄罗斯钯金征收的关税可能会在电动汽车生产中产生对铂金的溢出需求。

- 欧洲、中国和美国氢基础设施投资的步伐和重型汽车的采用率。

- 中国的珠宝需求可能会发挥作用。仅用1%的黄金替代品就可以使铂金赤字扩大全球供应量的10%。

%20(1).jpg)

在过去两周里,白银市场经历了极端剧烈的震荡与高位博弈:价格一度快速攀升至历史极高水平,随后出现剧烈回落,反映出市场在避险情绪、基本面需求与投机力量之间的动态平衡。这一阶段白银的表现不仅成为贵金属市场的焦点,也凸显出当前全球经济风险偏好和宏观预期的复杂变化。

一、价格表现:高峰与震荡并存

自年初以来,白银价格持续上涨,并在近期迎来非常显著的高点突破。本周一,白银价格在近段时间内冲高至历史高位——一度触及每盎司约 117.75 美元 的峰值水平,盘中涨幅一度接近 14%,创下自2008年以来的最大单日涨幅。上涨之后的价格快速回落,最终在震荡中收复1%涨幅收盘。反映出,在连续多日由动量推动、追涨情绪主导的行情之后,这轮上涨已经变得相对脆弱。

同一时间段内,黄金虽也创新高,但白银的价格波动要更加剧烈,表现出更高的弹性和交易热度。国内市场对应的沪银主连合约也在本轮行情中刷新了历史高点,盘中涨幅显著。

二、推动白银上涨的核心因素

白银价格在这两周内的大幅波动并非偶然,它是多重基本面与市场情绪因素共同作用的结果:

1. 全球供需高度紧张

从供给端看,全球白银市场已连续多年处于供给短缺状态。截至最近数据(约 2025 年末),白银产量约 3.18 万吨,而实际需求达到了约 3.55 万吨,现实中每年存在接近 8 亿盎司的累计缺口。供应端无法快速响应需求增长,因为全球大部分白银是伴生矿产品,其生产扩张依赖于铜、铅锌矿的开发节奏,且新矿开发周期长达 5–10 年。供给结构的僵化,成为白银价格持续上行的重要基本面支撑。

此外,即使在高价区间,工业消费仍保持强劲,特别是在新能源、光伏、电子设备等领域对白银的需求持续增长,这进一步加剧了供应紧张的局面。

2. 避险需求与宏观不确定性

宏观经济的多重不确定性是近期贵金属走强的重要逻辑背景之一。通胀预期、货币政策路径的不确定性、全球地缘风险等因素,使白银不仅具备避险功能,还因其对市场情绪敏感而呈现高波动性。今日,美国对韩国商品提高关税至25%,以及市场对美联储政策和主席人选的猜测,加剧了投资者的不确定性。此外,财政支出和货币政策压力也促使部分资金从债券和货币资产转向贵金属,形成所谓的贬值交易。

3. 美元与利率预期影响

美元走势与美国货币政策预期对贵金属价格影响显著。随着市场对美联储未来可能降息的预期升温,以及美元在多重政策不确定性下有所承压,白银作为非收益资产吸引了更多资产配置需求。这种“美元弱、避险升”组合在贵金属市场整体放大了资金对价格上行的共振。

三、短期震荡与风险提示

此次白银行情的一个明显特征是急涨之后伴随急跌与回撤,反映出市场对“过热状态”的风险意识正在增强。

分析人士认为,这种极端振幅表明白银部分上涨动力已接近短期极限,且高企价格开始对工业使用产生“挤压”效应,迫使光伏等行业加速寻求替代材料,从而削弱部分实需支撑。这种供需博弈下的潜在阻力,是当前白银短期回落不可忽视的风险因素。

虽然工业需求是白银的基本面支撑之一,但高价会对需求端形成反压。例如光伏等行业可能加快替代材料布局,减少对白银的边际需求,这在极端高价位很可能削弱部分基本面支撑,从而影响中长期供需平衡。

四、未来走势展望

从长期供需基本面来看,白银的结构性紧张、工业需求增长与避险功能并存,为其价格中枢提供了较强支撑。只要这些基本因素未发生根本性逆转,白银在未来阶段仍有潜力维持高位波动。

不过,从技术面和市场情绪出发,高位的急速上涨属于典型的“爆发型行情”,短线极易出现回调或震荡加剧,特别是在遇到宏观数据或全球金融风险事件时,价格波动可能进一步放大。

因此,在关注白银中长期上涨逻辑的同时,需要警惕短期波动风险,避免在高位盲目追涨,并重点关注供需基本面数据、美元走势和全球避险情绪的变化。

总结

基本面供需紧张、工业需求增长和宏观不确定性构成了白银中长期支撑,价格快速透支上涨动能,叠加高位获利了结与需求端压力,短期波动风险显著,需要投资者保持谨慎。

FX markets enter an important window with a Federal Reserve policy decision and press conference, US ISM activity data, German inflation releases, China PMIs, and Australian labour figures all due.

Quick facts

- The upcoming Fed policy decision and press conference are closely watched for guidance on the potential timing of rate cuts, with implications for US Treasury yields and USD direction.

- Broad USD selling has intensified over the last 48 hours. The move has coincided with renewed tariff rhetoric and heightened sensitivity to FX intervention narratives.

- ISM Manufacturing PMI is scheduled for Monday, 2 February, with ISM Services PMI on Wednesday, 4 February, providing timely insight into US growth momentum.

- German CPI, euro area GDP and unemployment, China PMIs, and Australian labour data provide regional context, particularly for EUR and AUD crosses.

USD/JPY

What to watch

The Federal Reserve decision and subsequent press conference are key events influencing US Treasury yields.

Any shift in tone around inflation progress, economic risks, or rate cut timing expectations may affect yield differentials and near-term USD sensitivity.

Recent broad USD weakness, reinforced by tariff-related headlines and intervention sensitivity, has added downside pressure to the USD.

On the JPY side, Japan inflation signals, including Tokyo CPI, are relevant as indicators of domestic price trends and potential policy direction.

Key releases and events

- Thu 30 Jan: Japan Tokyo CPI (January)

- Thu 30 Jan: Federal Reserve policy decision and press conference

- Mon 2 Feb: US ISM Manufacturing PMI

- Wed 4 Feb: US ISM Services PMI

Technical snapshot

USDJPY has broken lower from its recent consolidation zone, with downside range evident over the last 48 hours. Price has moved down to the 200-exponential moving average (EMA) and is testing a level not seen since October 2025.

EUR/USD

What to watch

The Fed decision and press conference may influence EUR/USD primarily through USD moves linked to Treasury yield reactions.

On the EUR side, German CPI will show inflation trends, while euro area flash GDP and unemployment data inform the regional growth outlook.

Key releases and events

- Thu 29 Jan: Germany CPI (preliminary)

- Thu 29 Jan: Eurozone flash GDP, Q4 2025

- Thu 30 Jan: Federal Reserve decision and press conference

- Fri 30 Jan: Eurozone unemployment rate

Technical snapshot

EURUSD has extended above a prior resistance level, with expanded daily ranges and strong momentum. Price action in other USD crosses suggests the move may be reflecting USD weakness, rather than a material shift in euro area fundamentals.

EUR/AUD

What to watch

Alongside euro area growth numbers, Australian employment data may influence near-term EUR/AUD sensitivity ahead of the RBA policy decision next week.

China's official PMIs remain relevant, as shifts in Chinese activity expectations can influence AUD via commodity demand and regional risk sentiment.

Key releases and events

- Thu 29 Jan: Australia Labour Force, Detailed (Dec 2025), 11:30am AEDT

- Fri 31 Jan: China official Manufacturing and Non-Manufacturing PMIs

- Tue 4 Feb: RBA policy decision

Technical snapshot

EUR/AUD has decisively broken below its prior support zone, with price now testing levels not seen since April 2025. Momentum remains negative, consistent with a renewed downside phase rather than consolidation.

Bottom line

The Fed decision and press conference, US PMI data, German inflation releases, China PMIs, and Australian labour figures are clustered in a short window.

Markets will be watching whether the USD weakness evident over the last 48 hours extends further.

Expected earnings date: Thursday, 29 January 2026 (US, after market close) / early Friday, 30 January 2026 (AEDT)

Key areas in focus

iPhone

The iPhone remains Apple’s largest revenue driver. Markets are likely to focus on unit demand, product mix (including higher-end models), and any signals on upgrade momentum and regional trends.

Services

Investors are likely to focus on growth across areas such as the App Store, iCloud, Apple Music and other subscriptions, alongside any commentary on average revenue per user (ARPU). The size and engagement of Apple’s installed base remain central to overall performance.

Wearables, home and accessories

This segment includes products such as Apple Watch, AirPods, Beats headphones, home-related devices, and accessories. Investors are likely to watch revenue trends in this segment as an indicator of discretionary consumer demand.

Cost and margin framework

Management has flagged tariff and component cost pressures in prior commentary. Markets may remain sensitive to gross margin commentary and any signals of incremental cost pressure or mitigation strategies.

What happened last quarter

Apple’s most recent quarterly update (fiscal Q4 2025) highlighted record September-quarter revenue and EPS, alongside record Services revenue and continued emphasis on installed-base strength.

The prior update also included discussion of holiday-quarter expectations and cost headwinds (including tariffs), which have influenced expected margins and management guidance.

Last earnings key highlights

- Revenue: US$102.5 billion

- Earnings per share (EPS): US$1.85 (diluted)

- iPhone revenue: US$49.03 billion

- Services revenue: US$28.75 billion

- Net income: US$27.5 billion

How the market reacted last time

Apple shares rose in after-hours trading following the release, as investors assessed the results against analyst expectations and management’s holiday-quarter commentary, including tariff-related cost pressures and regional demand considerations.

What’s expected this quarter

Bloomberg consensus points to year-on-year EPS growth, with markets also focused on the revenue outcome and gross margins, given the scale and importance of the holiday quarter for Apple’s earnings profile.

Bloomberg consensus reference points (January 2026):

- EPS: about US$2.65

- Revenue: about US$138 billion

- Full-year FY2026 EPS: about US$8.1

*All above points observed as of 26 January 2026.

Expectations

Sentiment around Apple may be sensitive to any disappointment on holiday-quarter revenue, Services momentum, or margin commentary, given the stock’s large index weight and the importance of this reporting period.

Listed options were implying an indicative move of around ±3% to ±4% based on near-dated, at-the-money options-implied expected move estimates observed on Barchart at 11:00 am AEDT on 25 January 2026. Implied volatility was approximately 29% annualised at that time.

These are market-implied estimates (not a forecast) and may change. Actual post-earnings price moves can be larger or smaller.

What this means for Australian traders

Apple’s earnings can influence near-term sentiment across major US equity indices, particularly Nasdaq-linked products, with potential spillover into the Asia session following the release.

Important risk note

Immediately after the US close and into the early Asia session, Nasdaq 100 (NDX) futures and related CFD pricing can reflect thinner liquidity, wider spreads, and sharper repricing around new information.

Such an environment can increase gap risk and execution uncertainty relative to regular-hours conditions.

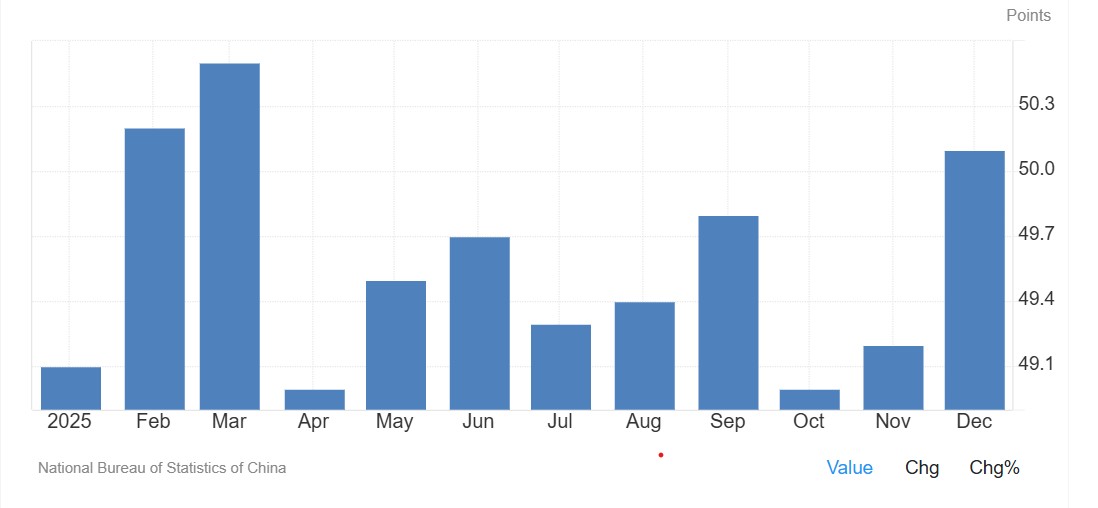

Asia-Pacific markets head into the week with Australia’s CPI as the key domestic catalyst, Japan’s month-end inflation and activity data keeping JPY and equities in focus, and China’s official PMI providing an important read on regional growth momentum.

Quick facts

- China: NBS manufacturing PMI rose to 50.1 in December 2025. Consensus for Saturday’s release is 50.2.

- Australia: CPI, Australia (Dec) is the key local catalyst, with implications for rate expectations and AUD pricing.

- Japan: Tokyo CPI and month-end labour/activity data keep USD/JPY and Nikkei futures in focus following last week’s BoJ meeting.

- Global backdrop: US earnings momentum, US CPI expectations and geopolitical developments remain secondary but relevant drivers for Asia-Pacific risk sentiment.

China

Attention turns to China’s official PMI after December’s improvement saw the PMI move back above 50—a level commonly interpreted as expansion in the survey, though month-to-month readings can be volatile.

Consensus suggests a rise to 50.2; if met, it may help reinforce the view that growth momentum is stabilising into early 2026.

Key release

- Sat 31 Jan: NBS manufacturing and non-manufacturing PMI (Jan)

How markets may respond

- Regional equities and risk: Sustained PMI readings above 50 could support broader Asia risk appetite and materials-linked sectors. A reversal below 50 may temper recent optimism.

- AUD spillover: China-sensitive assets, including the AUD and materials stocks on the ASX, may react alongside domestic CPI outcomes.

Japan

Following last week’s BoJ meeting, focus shifts to Tokyo CPI and month-end activity data. These releases late in the week may shape near-term expectations around Japan’s inflation trajectory and the tone of the dataflow.

Key events

- Thu 29 Jan: Tokyo CPI (Jan) (medium sensitivity)

- Fri 30 Jan: Japan unemployment (Dec), retail sales (Dec), industrial production (Dec) (medium sensitivity)

How markets may respond

- USD/JPY: Month-end inflation and activity data can drive front-end rate repricing, with USD/JPY remaining a key transmission channel.

- JP225 (Nikkei futures): The contract has recently traded in a defined range. Market participants may monitor the ~54,250 area on the upside and ~52,250 on the downside as reference points, with price action around these levels often used to gauge whether the range is persisting.

Australia

Australia’s week is dominated by the CPI release. The outcome may influence rate expectations, with the next scheduled RBA decision still in the balance.

ASX 30 Day Interbank Cash Rate Futures imply around a 56% probability of a cash-rate increase at the next scheduled RBA decision (implied pricing can change quickly and is not a forecast).

AUD pricing is likely to remain sensitive alongside broader global risk conditions.

Key release

- Wed 28 Jan: CPI, Australia (Dec) (high sensitivity)

How markets may respond

- ASX 200: Rate-sensitive sectors may react more to the policy implications than the headline CPI number, particularly given recent strength in materials.

- AUD/USD: CPI outcomes may influence whether AUD/USD sustains around/above its current zone or drifts back toward prior trading ranges.